Market update from Lloyd & Whyte: How are your investments performing?

14/05/2021

14/05/2021

The first quarter has flown by and it seems investors are confident that economies are on the road to recovery. This assumes the global vaccine roll-out is effective and that we all get back to something approaching normal as the year progresses. This sentiment is having a positive effect on some asset classes within our investment portfolios, particularly equity assets (shares in companies), where demand has been strong.

This demand has been fuelled by the expectation of significant fiscal support in the US and Europe with this stimulus resulting in improved economic growth expectations. This support is good news for equity investors, but a consequence of this has not been so good for investors in fixed interest securities (frequently referred to as ‘Bonds’).

It is often said that investment markets have already ‘priced in’ future events. This sometimes turns out to be true, sometimes it isn’t. At the moment investment markets are weighted towards the expectation of very strong economic growth but the concern is this could see some economies overheating! A classic case of where demand outstrips supply. This would lead to a rise in inflation and the possibility that central banks may decide to increase interest rates sooner than expected to control this. These potential outcomes will have consequences for fixed interest securities, as they generally have fixed annual coupons (regular interest payments) and a pre-determined maturity date when the capital invested is returned. The structure of bond assets means an increase in inflation would erode the value of the regular interest payments, as well as the capital value at maturity. If interest rates were increased it would further lower bond prices, which is unhelpful for bondholders, but potentially attractive to new investors.

Fixed interest securities feature in most investment portfolios as they generally offer a lower risk alternative to equity assets, they are structured differently, and they usually react differently to economic conditions. This diversity helps manage some of the investment risk, although we are currently seeing bond values being affected by these inflationary and interest rate concerns. This resulted in a rotation out of bond investments during the quarter with this drop in demand seeing bond prices falling. Equity assets were the benefactor with the reflationary environment good for these assets.

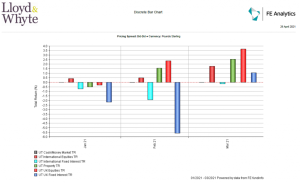

The bar chart below provides a general overview of the performance of the main asset classes during January, February, and March. It shows the discrete performance for each month (from the start to the end of the month) and reports the total return, which assumes any interest or dividends are reinvested in pounds sterling. The blue bars are the fixed interest assets (bonds) both UK and International with the red bars showing UK and International equites. The cash bar at the start of each month is flat and virtually indistinguishable with property represented by the green bar.

The chart shows how fixed interest assets have fared in comparison to other assets, particularly equities. Although this is a relatively short period it also highlights the generally uncorrelated relationship between equities and bonds and the benefits of combining these in investment portfolios.

Looking ahead central banks will want to maintain interest rates at low levels in order to be able to service the significant amount of debt within their economies. This is going to be a key issue assuming the global vaccine roll out delivers the outcome we are all hoping for and governments successfully navigate their way out of lockdown. If this happens, it is anticipated that pent up demand for goods and services will result in a temporary uplift in inflation. The conundrum for central banks may occur if economies were to grow too quickly and use up all the available supply, they may have to look at increasing interest rates to cool demand.

This situation has been rumbling on for a few months with speculation about the potential outcome swaying investor sentiment. Bond assets are an essential part of risk managed long term investment strategies. They have strong defensive qualities and play a pivotal role in maintaining a balance of diverse asset holdings within investment portfolios. At the moment it is the asset class that is most under scrutiny and to put it into context, it was just over a year ago that bonds assets helped support portfolio values as equities plummeted in the first wave of the pandemic.

It is sometimes difficult to shut out the short term ‘noise’ surrounding investments and this recent issue is one of many that will be encountered during the investment journey. This will have affected the reporting value of some portfolios, although all the speculation driving this may not materialise and it is why we remain focused on long term objectives.

As a valued client of Lloyd & Whyte we are here to discuss any queries about your investments. Our Independent Financial Advisers are happy to chat about your current or future investment plans.

Other articles you should read:

Reflecting on your past finances to secure the future

Key Points of the Spring budget 2021

Hopes of a “swifter and more sustained economic recovery”

Why it pays to update your pension expression of wishes

Every piece of jewellery tells a story…

Vaccines put a spring in investors’ step

Lloyd & Whyte (Financial Services) Ltd are authorised and regulated by the Financial Conduct Authority. It is important to take professional advice before making any decision relating to your personal finances. Information within this newsletter is based on our current understanding of taxation and can be subject to change in future. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK; please ask for details. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. If you withdraw from an investment in the early years, you may not get back the full amount you invested. Registered in England No. 02092560. Registered Office: Affinity House, Bindon Road, Taunton, Somerset, TA2 6AA Calls may be recorded for use in quality management, training and customer support.