5 Minute Market update: How are your investments performing?

13/08/2021

13/08/2021

The main theme affecting investment markets since the start of 2021 has been the fear of inflation. The success of the vaccination roll-out which is prevalent in developed economies has greatly assisted the easing of Covid-induced restrictions and led to increased consumer spending. This has helped these regions make strong economic recoveries and pushed up year-on-year inflation from the artificially low levels we saw during last year’s lockdown.

Investors remain concerned that rising inflation could lead to central banks increasing interest rates which is particularly sensitive for fixed-interest assets (often referred to as bonds), especially Government bonds. The prices of these share an inverse relationship with interest rates, so a rise in interest rates means a fall in bond prices and their reporting value. This has resulted in bond assets falling out of favour with equity assets benefitting.

Speculation about interest rates rising has continued to rumble on throughout the first half of 2021, with some investors feeling that the strong financial support governments are providing to their respective economies is helping to fuel price increases. This may put extra pressure on central banks to curb consumer spending by increasing the cost of borrowing by raising interest rates. Although it is worth noting that the recent statements made by leading central banks confirms they believe the uplift in inflation is temporary. They see these recent increases as transitionary (whilst the supply of goods and services return to normal levels) and because of this it would appear that there is unlikely to be any imminent uplift in interest rates.

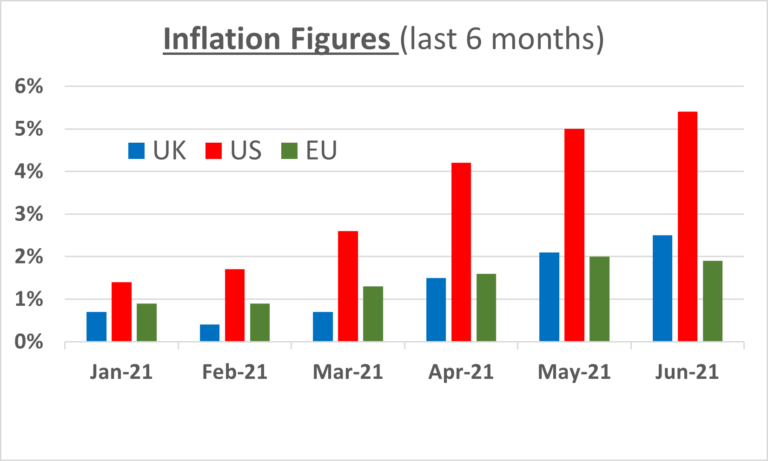

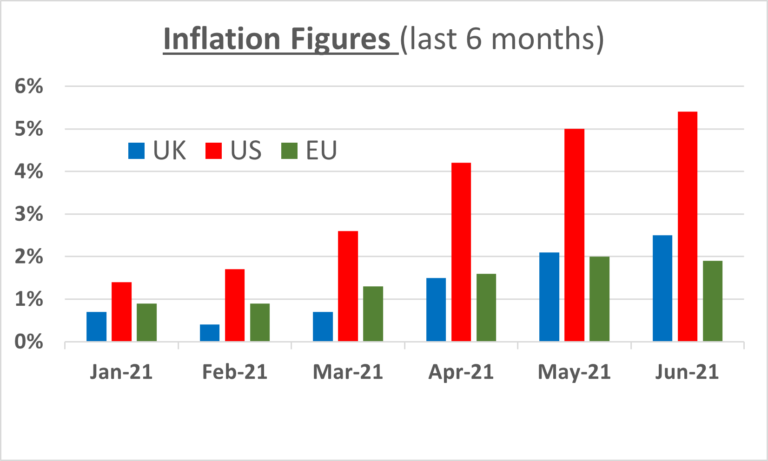

The chart below shows the upward trend in inflation figures from UK, US and EU regions over the last six months. (information obtained from the Trading Economics website at https://tradingeconomics.com/ ).

Speculation is an inherent feature in financial markets and it will continue to drive sentiment and trading activity. Financial markets will remain sensitive to the possibility of sustained higher inflation or whether this does in fact turn out to be a temporary trend.

During the second quarter, economic data, particularly in the developed regions, has generally been good and beneficial for investment markets. Bond prices started to improve, as demand increased, with investors apparently more accepting of the reassurances given by central banks (even though they have some way to go to recover the falls seen in the first quarter).

The success of the vaccine roll-out in developed regions has been helpful for equity markets with these experiencing a shift in the companies and sectors investors are favouring. At the start of the year ‘value stocks’ were in favour as investors plumped for companies that appeared to be trading below their real worth with the current trend favouring more ‘growth’ focused companies that offer strong earnings potential. One of the benefits of investing in a diverse portfolio is that your money will be exposed to these differing investment styles and consequently well-positioned to cater for the changes in trend that markets experience.

It is pleasing to report that our portfolios have performed in line with our expectations during 2021 with those further up the risk scale benefitting from current trading conditions. As investors, we tend to focus on the near term and consequently place too much emphasis on current issues, however we do know that these things generally even out over the medium to longer term. That said we have experienced an extraordinary global pandemic that we hope won’t be repeated, and although things appear to be improving, it is sensible to remain mindful that Covid variants still have the potential to disrupt as we aim to return to something resembling normal. The second half of the year is likely to continue in a similar vein with inflationary and infection rates swaying market sentiment.

***

Jeff Bailey is the author of this article and the Technical Manager for Lloyd & Whyte’s team of Independent Financial Advisers. As always if you have any concerns about your investment arrangements, or there has been a change in your circumstances, please contact your adviser on 01823 250750

It is important to take professional advice before making any decision relating to your personal finances. Information within this newsletter is based on our current understanding of taxation and can be subject to change in future. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK; please ask for details. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. If you withdraw from an investment in the early years, you may not get back the full amount you invested.

Lloyd & Whyte (Financial Services) Ltd are authorised and regulated by the Financial Conduct Authority. Lloyd & Whyte Ltd is registered in England No. 03686765. Lloyd & Whyte (Financial Services) Ltd is registered in England No. 02092560. Registered Office: Affinity House, Bindon Road, Taunton, Somerset, TA2 6AA. Calls may be recorded for use in quality management, training and customer support.