How are your investments looking at the end of 2021? What is happening in the markets?

09/12/2021

09/12/2021

Another quarter has flown by and we are only a few weeks away from Christmas. Economies continue to wrestle with supply issues and manufacturers in certain sectors are finding it difficult to replenish their stock (demand is high) as they focus their efforts on keeping up with current orders.

The microchip industry is a prime example of this with the pandemic seeing an increase in the use of electronic goods for communication and home schooling. These depleted stocks which haven’t yet been replaced means that we are seeing manufacturers struggling to fulfil new orders.

The demands of the festive season will add pressure and is likely to result in a shortage of sought-after goods, which will see prices rise.

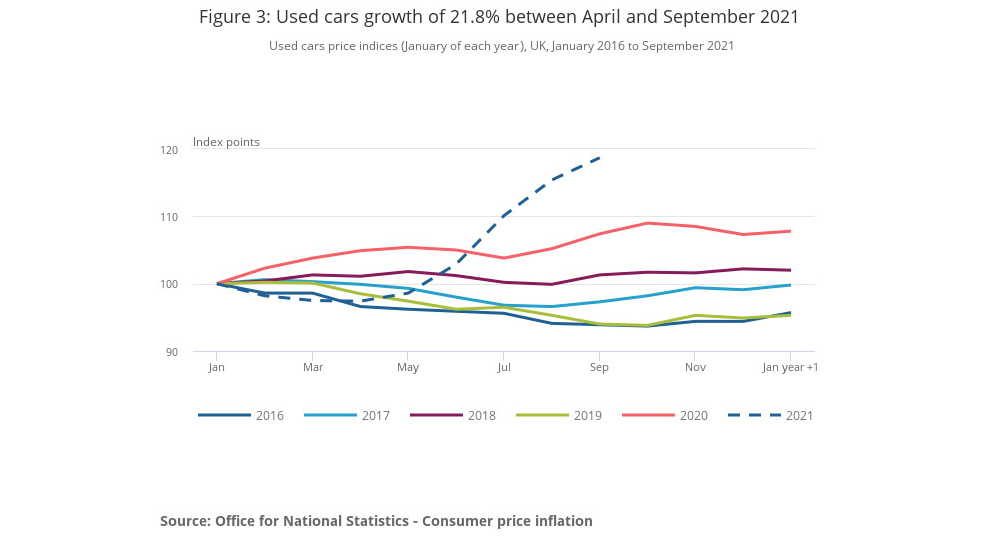

This demonstrates a fairly simplistic look at the two sides of the inflationary pressures economies are experiencing, with a lack of supply at a time of increased demand, resulting in price increases. An example of this can be seen in the line chart below. This shows the index tracking used car prices over the last five years. By overlaying the index performance of each year, starting in January with an index level of 100. Clearly, 2021 is showing prices picking up very quickly from May onwards as dealerships reopened following lockdown and demand for new cars quickly depleted stock levels. Dealers were unable to replace these, due to a shortage of semiconductors affecting new car production and it turned consumers to the used car market. Probably not the best time to buy if you are looking for a bargain.

Supply chain difficulties in certain sectors is feeding through to inflation figures and with demand remaining high, it is clearly a concern for central banks. Their current thinking suggests the uplift we have seen in inflation, albeit from artificially low starting values during lockdown, may not be as temporary as originally thought. This increases the likelihood of interest rate rises with the first of these potentially happening just before Christmas and a further rise expected to follow in the New Year.

The good news is that financial markets have generally factored these rises into current values, as central bank policy is to communicate their thinking beforehand.

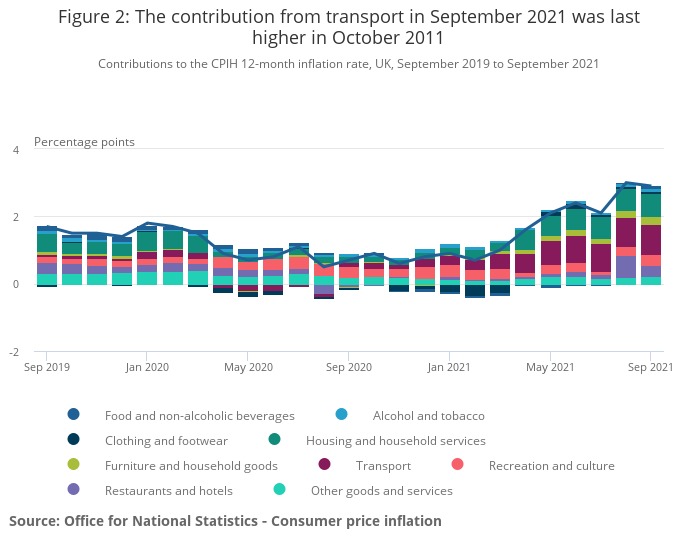

The effect of interest rate increases is used to help slow down the pace of economic expansion by reducing consumer spending. The chart below shows the Consumer Price Index including housing costs (CPIH) which highlights the significant contribution to inflation from transport and housing costs. This is something we can all relate to with higher energy and fuel prices noticeably affecting us.

You may have heard the expression that investments “climb a wall of worry”. This is where financial markets show resilience despite economic or political news that may otherwise lead to a market sell-off. This is generally what has been happening this year with regards to inflation and interest rates. This theme has been rumbling on since the start of the year with businesses affected by higher costs and some struggling to recruit following Brexit.

Taking these things into account it is pleasing to note that our portfolios have performed in line with expectations with equity assets (shares in companies) helping to support interest rate sensitive bond assets, which have had a “bumpy ride” so far this year. Looking ahead the Inflation/interest rate concerns, supply chain and recruitment issues will continue to drive short-term market sentiment, however, we remain confident the diverse positioning within our portfolios will continue to deliver their outcome objectives.

As always your Independent Financial Adviser is on hand to discuss any questions you may have regarding your investments.

It is important to take professional advice before making any decision relating to your personal finances. Information within this newsletter is based on our current understanding of taxation and can be subject to change in future. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK; please ask for details. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. If you withdraw from an investment in the early years, you may not get back the full amount you invested.